I. Industry Core: Material Classification and Application Atlas

Magnetic materials are indispensable "functional cornerstones" of modern industry, primarily divided into two pillars:

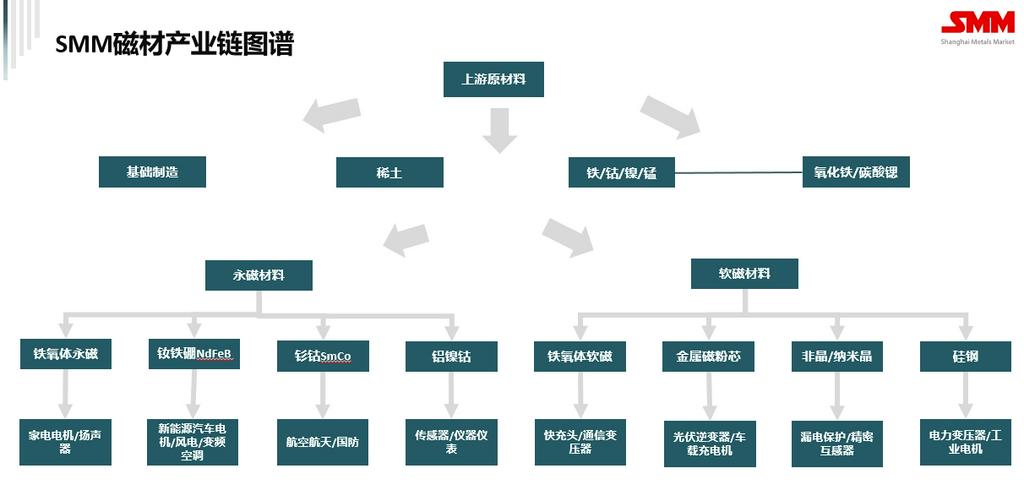

Permanent Magnetic Materials: Once magnetized, they retain high magnetism for extended periods (high coercivity, high remanence), serving as the core medium for electrical-to-mechanical energy conversion.Ferrite Permanent Magnets: (Main composition: SrO·6Fe₂O₃ or BaO·6Fe₂O₃) The most widely used and cost-effective, accounting for over 75% of global production (by weight). Key applications: automotive motors (wipers, starter motors, etc.), home appliance motors (air conditioners, refrigerator compressors, vacuum cleaners, etc.), power tools, and speakers.

NdFeB: (Main composition: Nd₂Fe₁₄B) Known as the "Magnetic King," with BH far exceeding ferrites and a wide adjustable performance range. Dominates the high-performance permanent magnet market. Core applications: NEV traction motors (critical for high-speed and lightweight design), wind turbine generators (direct-drive/semi-direct-drive permanent magnets), inverter air conditioner compressors, energy-saving elevator traction machines, high-end consumer electronics (e.g., smartphone linear motors, TWS earphones), and industrial robot servo motors.

SmCo: Exhibits excellent high-temperature and corrosion resistance but is costly (contains strategic metal Co). Primarily targets high-end sectors: aerospace (actuators, navigation), defense (radar, missile guidance), high-temperature oil drilling equipment, and high-end sensors. Market share is relatively small.

AlNiCo: The oldest permanent magnet, with good high-temperature stability and high magnetic induction but low coercivity. Mainly used in traditional fields like sensors and electroacoustic devices.

Soft Magnetic Materials: Feature low coercivity, enabling easy magnetization and demagnetization. They are pivotal for electrical-to-magnetic-to-electrical energy conversion and regulation, with core characteristics being high permeability and low loss.

Ferrite Soft Magnets: (Main composition: MnZn, NiZn) High resistivity and low high-frequency loss. Foundational applications: high-frequency switching power supplies (e.g., smartphone fast charging adapters, PC power adapters), high-frequency transformers, broadband communication (network transformers, RF components), electromagnetic compatibility (EMI filters), and induction heating equipment.

Metal Soft Magnetic Powder Cores: (Composed of iron silicon, iron silicon aluminum, iron nickel molybdenum, amorphous/nanocrystalline powders + insulation coating + compression) High saturation magnetic flux density, low loss, and excellent DC bias capability.Core Applications: PFC inductors and output filter inductors in large power inverters and frequency converters (PV inverters, on-board chargers (OBCs) for NEVs, Power Conversion Systems (PCS)), server power supplies, etc.

Amorphous and Nanocrystalline Alloys: (e.g., Fe-based, Co-based) ultra-thin strips with extremely low high-frequency losses and high permeability. Primary Applications: precision current transformers, residual current circuit breakers (miniaturized/high-efficiency), high-frequency switching power supply transformers, electromagnetic compatibility components.

Electrical Steel: The most widely used soft magnetic material, "ancient" yet with vast applications. Core Applications: power transformers (core of transmission and distribution networks), cores for various motors/generators (industrial motors, home appliance motors).

II. Industry Landscape: Geographical Distribution and Clustering Trends

China has established the world's most comprehensive magnetic material industry chain, with absolute dominance in both production and consumption (e.g., accounting for over 90% of global sintered NdFeB production). Enterprise layouts exhibit significant geographical clustering:

Zhejiang: The core hub for the permanent magnet industry.

Ningbo Region: A global NdFeB powerhouse, home to top-tier enterprises such as Zhong Ke San Huan (a technology leader), Ningbo Yunsheng (combining technology and scale), and Jintian Magnetics.

Dongyang-Yiwu Region: The headquarters of DMEGC, a world-class ferrite magnetic material giant (permanent magnets + soft magnets), expanding into metal magnetic powder cores, PV, etc.

Hangzhou and Other Cities: Home to multiple soft magnetic ferrite and magnetic powder core enterprises.

Guangdong: The driving center for electronics manufacturing and applications.

Pearl River Delta (Shenzhen, Dongguan, Huizhou, etc.): A vast downstream electronics manufacturing industry cluster (home appliances, mobile phones, PCs, etc.), giving rise to numerous terminal-oriented magnetic material suppliers (primarily ferrite permanent magnets and soft magnets) and module manufacturers. The region boasts a large number of enterprises, with a significant presence of small and medium-sized enterprises.

Jiangxi (Ganzhou): Supported by the resource hinterland of the "Rare Earth Kingdom."

Ganzhou: Leveraging abundant medium-heavy rare earth resources, JL MAG Rare-Earth has established a robust NdFeB production site here, primarily targeting the NEV and wind power sectors, with significant upstream resource advantages.

Northern China (Beijing-Tianjin, Inner Mongolia): A focus on raw materials and specific sectors.

Baotou: Relying on China Northern Rare Earth (the world's largest supplier of rare earth raw materials), it has formed industries such as rare earth permanent magnets (e.g., Innuovo Magnetics under Innuovo) and rare earth alloys.

Beijing-Tianjin Region: Home to technology-leading enterprises such as Antai (a long-established comprehensive enterprise engaged in amorphous, nanocrystalline, and NdFeB production and R&D) and Zhenghai Magnetic Material (specializing in high-performance NdFeB with significant advantages in the NEV sector), the area also hosts national-level R&D institutions like China Iron & Steel Research Institute.

Shandong: Yantai Zhenghai Magnetic Material (a key base for high-performance NdFeB).

Central and Western Regions (Shanxi, Sichuan, etc.): Focused on raw materials and some low and mid-end manufacturing, such as certain ferrite material plants in Shanxi.

III. Competitive Landscape: Polarization and Breakthrough

The industry exhibits a "pyramid-shaped" competitive structure with increasing polarization:

High-end Segment: Represented by high-performance NdFeB (especially grades requiring high coercivity and operating temperatures) and specialty soft magnetic materials (high-performance powder cores, nanocrystalline). Key competitors include leading publicly listed firms or large conglomerates like JL MAG Rare-Earth, Zhenghai Magnetic Material, Ningbo Yunsheng, Zhong Ke San Huan, DMEGC (powder cores), Poco New Materials (powder cores), Dongmu Kedu (powder cores), and Antai (amorphous/nanocrystalline). These players typically partner with global top-tier clients (e.g., Tesla, BBA, Midea, Gree, Huawei, Sungrow, BYD, Goldwind Science&Technology), competing on technological barriers (grain boundary diffusion technology, refined grain control, uniform coatings), patent portfolios, product consistency, large-scale delivery capabilities, and upstream raw material control (especially rare earths). Market concentration is gradually increasing, with relatively strong profitability and rising localisation rates in mid-to-high-end applications (e.g., domestic firms now dominate wind power and NEV traction motors).

Low and Mid-end Red Ocean: Dominated by conventional ferrite permanent/soft magnets, mid-to-low performance NdFeB, and electrical steel. Comprising numerous small and medium-sized private enterprises (over 1,000 large-scale magnetic material producers nationwide), this segment faces brutal competition where price wars are the norm, technical thresholds are low, and structural capacity surplus is acute. Profit margins are severely squeezed by raw material price volatility and cost pressures. Survival hinges on economies of scale, refined management, or niche regional/sub-segment customer relationships.

IV. Technological Pulse: Innovation-Driven Future

The industry’s technological evolution centers on "higher performance, lower losses, enhanced stability, and reduced environmental dependency":

High-Performance Permanent Magnet Breakthroughs:

Industrialisation of High-Abundance Rare Earth (Ce-rich) Magnets: To reduce reliance on scarce Pr-Nd, Dy, and Tb in high-performance NdFeB, research intensifies on substituting or process optimization using more abundant Ce and La, lowering costs and ensuring supply chain security. Both the Chinese Academy of Sciences and relevant top-tier enterprises have made active deployments.

High-performance NdFeB without heavy rare earths (without Dy/Tb): Through grain refinement, grain boundary control, high-uniformity microstructure control, and other grain boundary diffusion processes (GBDP, with the core objective of reducing Dy/Tb usage or developing Dy/Tb-free formulations), combined with more advanced sintering technologies, it ensures sufficient high-temperature coercivity while significantly reducing the use of costly and strategically sensitive heavy rare earths. This has become the mainstream direction for industrialisation.

Improved thermal stability: Extreme operating conditions (such as in NEV motors and aerospace high-temperature environments) place higher demands on the thermal stability of magnets, with new-type additives and microstructure optimisation being key.

Evolution of soft magnetic materials towards high frequency and low loss:

High-performance metal magnetic powder cores: Developing powder core materials with higher saturation magnetic induction (Bs), lower high-frequency loss (Pcv), and higher DC bias capabilities (such as new-type FeNi systems, ultra-fine powders, and improved coating processes). Companies like Powdertech Advanced Material, KDM, and DMEGC are fiercely competing in this field.

Thinning and industrialisation of amorphous/nanocrystalline ribbons: Further improving production efficiency and consistency, reducing costs, and expanding applications in higher frequencies (above MHz) and high-precision current sensing.

Ferrite materials with low loss at high frequencies: Adapting to the increasing operating frequencies of 5G/6G communications, superfast charging, etc., with continuous optimisation of material formulations and processes.

Green and intelligent manufacturing:

Environmental protection processes: Reducing emissions of waste acid, wastewater, and dust, lowering power consumption, and developing green surface treatment alternatives (such as replacing phosphating and electroplating).

Digitalisation and intelligent manufacturing: Enhancing process control precision (batching, sintering), automation detection levels, and quality traceability capabilities to improve efficiency and consistency.

V. Challenges and the Future

Coexistence of opportunities and challenges:

Core challenges:

Security of upstream rare earth resources and price fluctuations: High-performance NdFeB is highly dependent on rare earth raw materials, particularly medium-heavy rare earths, with significant price fluctuations (evident from the peak in 2021-2022 and the correction in 2023). The security of the supply chain requires high attention. The issues of resource concentration and pricing power are looming threats.

Overcapacity in low and mid-end segments: Vicious competition in traditional fields such as ferrite materials has driven down industry profit margins, posing significant pressure for transformation and upgrading.

International Competition in High-end Fields: Japanese and European enterprises still hold leading advantages in certain top-tier applications (such as cutting-edge medical equipment and precision instruments) and core patents.

Accelerated Technological Iteration: Technological barriers are continuously rising, necessitating sustained increases in R&D investment.

Development Path and Recommendations:

Strengthening Upstream Integration: It is crucial for magnetic material enterprises (especially permanent magnet enterprises) to vertically extend their resource layouts (by deeply binding with rare earth groups or, like the Jinli model, locating near resources) or enhance their recycling and reuse capabilities.

Focusing on High-value Sectors: Enterprises need to clarify their strategic positioning. Top-tier enterprises should continuously strive for the highest end and increase their global market share, while small and medium-sized enterprises should excel and strengthen in niche areas or seek integration.

Technological Innovation-driven: Increase R&D investment in core technologies such as high-abundance rare earth magnets, next-generation soft magnetic materials, and intelligent manufacturing.

Embracing Green and Low-carbon: Magnetic materials play a pivotal role in the new energy revolution, and their production processes must also align with the "dual carbon" goals.

Collaborative Innovation in the Industry Chain: Strengthen cooperation between magnetic material enterprises and leading downstream application companies (such as motor manufacturers and complete machine manufacturers), equipment manufacturers, and research institutes to jointly define future needs and technological pathways.

------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Thank you for reading this far, for looking at the previous diagrams, and for enduring so much text to finally listen to me ramble on. When I wrote this article, the office was empty, with only me still typing away at the keyboard.

I've been thinking about how to start my first article on rare earths and how to inform the teachers and partners who helped me in the [hydrogen energy field] that ["Hi, I'm now looking into rare earth magnetic materials and motors. Hydrogen energy will be handled by my colleagues."]

Or, we could just skip the small talk and get straight to work. But I hope that you and I, the reader of this article, can be more than just colleagues—we can be friends who gossip and share our views on the world. More importantly, I want you to know that I take every task I'm responsible for seriously.

Whether it was hydrogen energy in the past, rare earth magnetic materials now, the domestic market currently, or the overseas market in the future, I've made an effort to understand every bit of knowledge and create every product I've wanted to make. I've poured 100% of my passion into every task.

Perhaps my current discussions on rare earth magnetic materials aren't that in-depth, and perhaps SMM doesn't have as much data on the development of magnetic materials and end-users. But please believe that I'll strive to do my best, just like when I first built the hydrogen energy industry data platform.

All that has passed is but a prelude; all that is to come is worth looking forward to. With that said, let's formally get to know each other:

This is Shi Xin, an analyst of rare earth magnetic materials at SMM. My phone number is 13515219405, and I'm responsible for analyzing the domestic magnetic material-motor market and overseas rare earth market. My WeChat ID is also 13515219405. If you're interested in this market and if I can be of help, please feel free to contact me.

I'm Sofia, an analyst of rare earth magnetic materials at SMM. Tel: 13515219405 (WeChat). I'm responsible for analyzing the domestic magnetic material-motor market and overseas rare earth market.

If you are interested in this market and if I can be of assistance, please feel free to contact me.